Waiting to Buy a Home?

Waiting to Buy a Home?

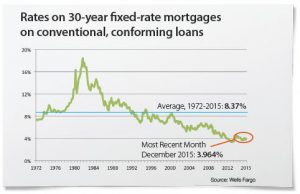

You May Miss out on Low Interest Rates

In December, the Federal Reserve raised the key interest rate by a quarter-point to range of 0.25% to 0.5%, the first rate increase in nearly a decade. 1 While some experts expect the Fed to raise rates gradually this year, some economists expect rates to increase three or four more times this year.2 Increases are anticipated to amount to a quarter-point each time, and when they do occur are subject to impact mortgage rates.2 What’s a homebuyer to do?

NOW IS THE TIME TO BUY!

While a quarter-point increase in interest rates doesn’t seem like much, it could mean the difference of hundreds of dollars a month in your mortgage payment. This will depend on the price of your home, your interest rate, how much you are borrowing and the size of your down payment. This is money you could use to renovate, go on vacation or save for retirement.3

WHAT SHOULD YOU DO NOW?

- Get pre-qualified for a mortgage if you haven’t done so already. Getting pre-qualified means you can spring into action when you find the home you want to buy. We work with great lenders in our area. If you’re looking for a lender you can trust, let us know and we’ll be happy to connect you with someone from our network.

- Narrow down your search criteria. What neighborhoods do you have your eye on? Do you want three or four bedrroms? Do you want a big yard or no yard at all? The list goes on and on. While buying a home is a process of selection, the more you know what you want, the better prepared you are to make the right decision.

- Get hunting. If you’ve been passively house hunting online, now is the time to ramp up your search. Let us know what you are looking for and we’ll work with you to find a great home that meets your criteria.

Sources:

Buffini & Company

1. CNN Money, December 16, 2015

2. The Guardian, January 6, 2016

3. Bankrate Mortgage Payment Calculator